All Categories

Featured

Table of Contents

This is despite whether the insured individual dies on the day the policy begins or the day prior to the plan finishes. In other words, the quantity of cover is 'degree'. Legal & General Life Insurance Coverage is an example of a level term life insurance plan. A level term life insurance plan can match a variety of conditions and needs.

Your life insurance policy plan can additionally create component of your estate, so can be based on Estate tax learnt more concerning life insurance policy and tax - 20-year level term life insurance. Let's consider some features of Life insurance policy from Legal & General: Minimum age 18 Optimum age 77 (Life Insurance), or 67 (with Important Ailment Cover)

What life insurance policy could you think about otherwise level term? Lowering Life Insurance Policy can assist safeguard a settlement home loan. The quantity you pay stays the same, but the level of cover decreases approximately according to the means a repayment mortgage lowers. Reducing life insurance policy can help your loved ones stay in the household home and stay clear of any additional disturbance if you were to pass away.

If you select level term life insurance coverage, you can budget plan for your costs since they'll stay the very same throughout your term. Plus, you'll recognize specifically how much of a survivor benefit your recipients will certainly receive if you pass away, as this quantity won't change either. The rates for degree term life insurance will depend on numerous factors, like your age, health and wellness standing, and the insurer you select.

As soon as you experience the application and medical exam, the life insurance coverage company will review your application. They ought to educate you of whether you have actually been approved shortly after you use. Upon authorization, you can pay your very first costs and authorize any kind of appropriate documentation to guarantee you're covered. From there, you'll pay your premiums on a regular monthly or annual basis.

What Are the Benefits of Level Benefit Term Life Insurance?

You can choose a 10, 20, or 30 year term and delight in the added peace of mind you deserve. Functioning with a representative can help you find a policy that works ideal for your demands.

As you look for ways to secure your financial future, you've most likely encountered a variety of life insurance policy options. Selecting the appropriate insurance coverage is a big decision. You desire to find something that will certainly aid sustain your loved ones or the causes vital to you if something takes place to you.

What Is Life Insurance Level Term? A Complete Guide

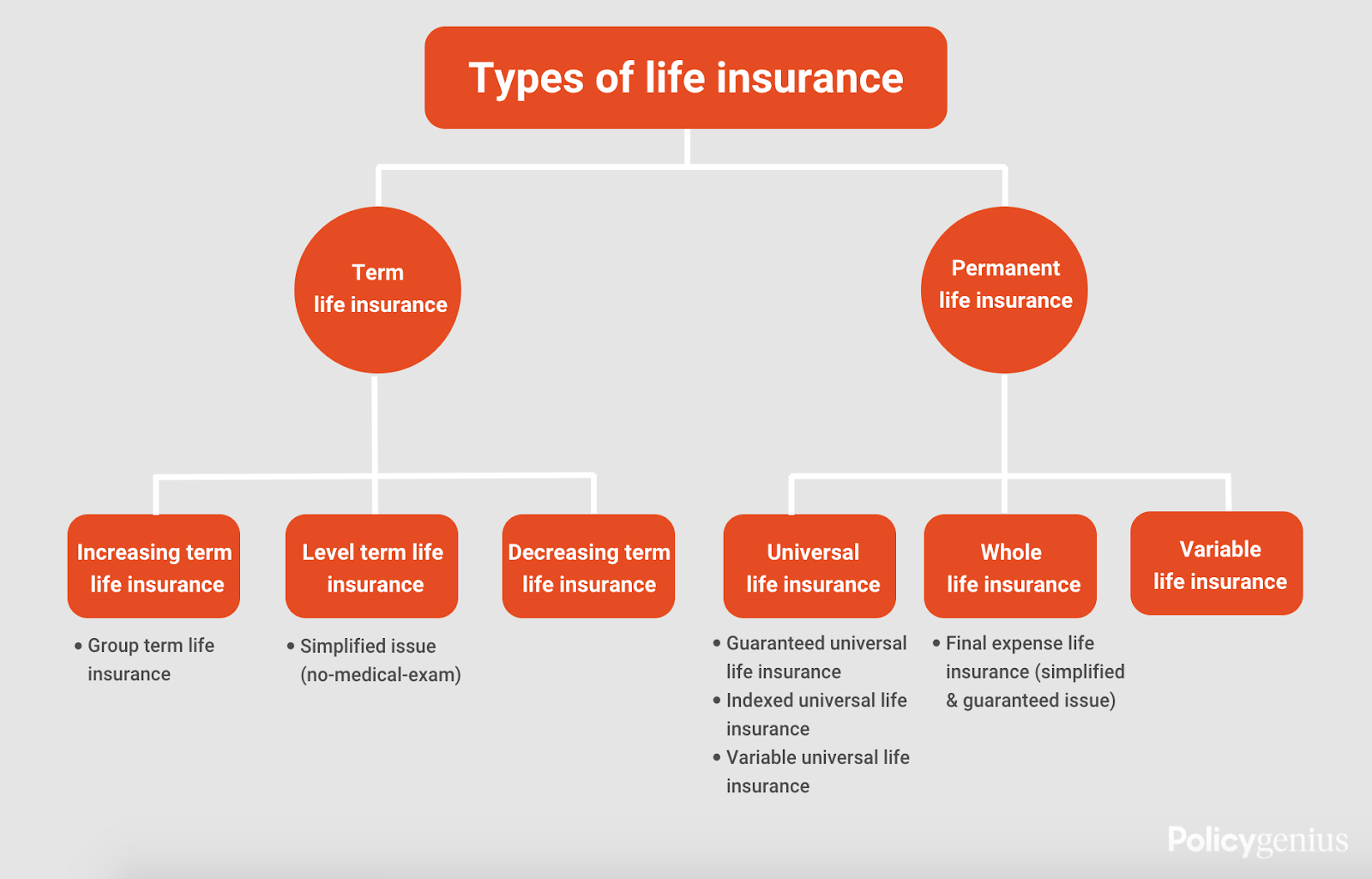

Many people favor term life insurance for its simpleness and cost-effectiveness. Term insurance policy contracts are for a reasonably brief, specified time period yet have choices you can customize to your needs. Particular advantage options can make your costs alter gradually. Degree term insurance coverage, however, is a kind of term life insurance policy that has consistent payments and an imperishable.

Level term life insurance policy is a subset of It's called "degree" because your costs and the advantage to be paid to your loved ones stay the same throughout the agreement. You will not see any changes in expense or be left questioning about its worth. Some agreements, such as yearly eco-friendly term, may be structured with costs that raise with time as the insured ages.

They're established at the beginning and continue to be the same. Having regular settlements can help you far better plan and budget plan due to the fact that they'll never ever alter. Dealt with survivor benefit. This is likewise established at the start, so you can recognize exactly what death benefit amount your can anticipate when you die, as long as you're covered and updated on premiums.

You agree to a set costs and fatality advantage for the period of the term. If you pass away while covered, your fatality advantage will certainly be paid out to liked ones (as long as your costs are up to date).

What is Voluntary Term Life Insurance? Pros and Cons

You might have the choice to for one more term or, much more likely, restore it year to year. If your contract has actually a guaranteed renewability stipulation, you might not require to have a new medical examination to keep your coverage going. Nonetheless, your costs are likely to enhance because they'll be based on your age at revival time.

With this alternative, you can that will last the rest of your life. In this instance, once again, you might not require to have any new medical tests, however premiums likely will rise due to your age and new protection (10-year level term life insurance). Various companies offer numerous choices for conversion, make certain to recognize your choices before taking this step

Speaking to an economic advisor likewise might assist you establish the path that aligns ideal with your total approach. The majority of term life insurance policy is level term throughout of the agreement duration, but not all. Some term insurance might feature a premium that rises gradually. With lowering term life insurance policy, your survivor benefit drops with time (this kind is typically obtained to especially cover a long-lasting debt you're repaying).

And if you're set up for renewable term life, then your costs likely will rise annually. If you're checking out term life insurance and desire to ensure simple and foreseeable financial protection for your family members, level term may be something to consider. As with any kind of kind of coverage, it may have some limitations that don't fulfill your needs.

How Does Level Premium Term Life Insurance Policy Work?

Commonly, term life insurance policy is extra cost effective than irreversible insurance coverage, so it's an economical means to secure monetary security. Versatility. At the end of your agreement's term, you have multiple choices to continue or carry on from protection, commonly without needing a medical examination. If your budget or protection needs modification, fatality benefits can be minimized gradually and cause a reduced premium.

Similar to other sort of term life insurance policy, once the contract finishes, you'll likely pay greater costs for insurance coverage due to the fact that it will recalculate at your existing age and wellness. Dealt with coverage. Level term uses predictability. If your monetary scenario adjustments, you might not have the required insurance coverage and could have to buy additional insurance.

That doesn't indicate it's a fit for everybody. As you're purchasing life insurance policy, here are a couple of vital factors to consider: Spending plan. Among the benefits of degree term protection is you recognize the expense and the fatality benefit upfront, making it simpler to without stressing over rises gradually

Age and health and wellness. Usually, with life insurance coverage, the healthier and younger you are, the even more budget friendly the insurance coverage. If you're young and healthy, it might be an attractive option to secure low costs now. Financial responsibility. Your dependents and economic responsibility play a role in determining your coverage. If you have a young family, for example, degree term can assist give financial backing during important years without spending for coverage longer than essential.

{kind=link}

Latest Posts

30 Year Term Life Insurance Instant Quotes

End Of Life Insurance Plans

Burial Insurance Reviews