All Categories

Featured

Table of Contents

Adolescent insurance coverage provides a minimum of defense and can offer coverage, which could not be offered at a later date. Quantities supplied under such protection are usually limited based upon the age of the kid. The existing limitations for minors under the age of 14.5 would certainly be the better of $50,000 or 50% of the amount of life insurance policy in force upon the life of the applicant.

Juvenile insurance coverage might be marketed with a payor benefit rider, which offers waiving future premiums on the kid's policy in the occasion of the fatality of the individual who pays the costs. Senior life insurance coverage, occasionally described as graded death advantage strategies, offers eligible older candidates with minimal entire life protection without a medical checkup.

The maximum issue amount of coverage is $25,000. These policies are normally much more expensive than a fully underwritten plan if the individual qualifies as a basic risk.

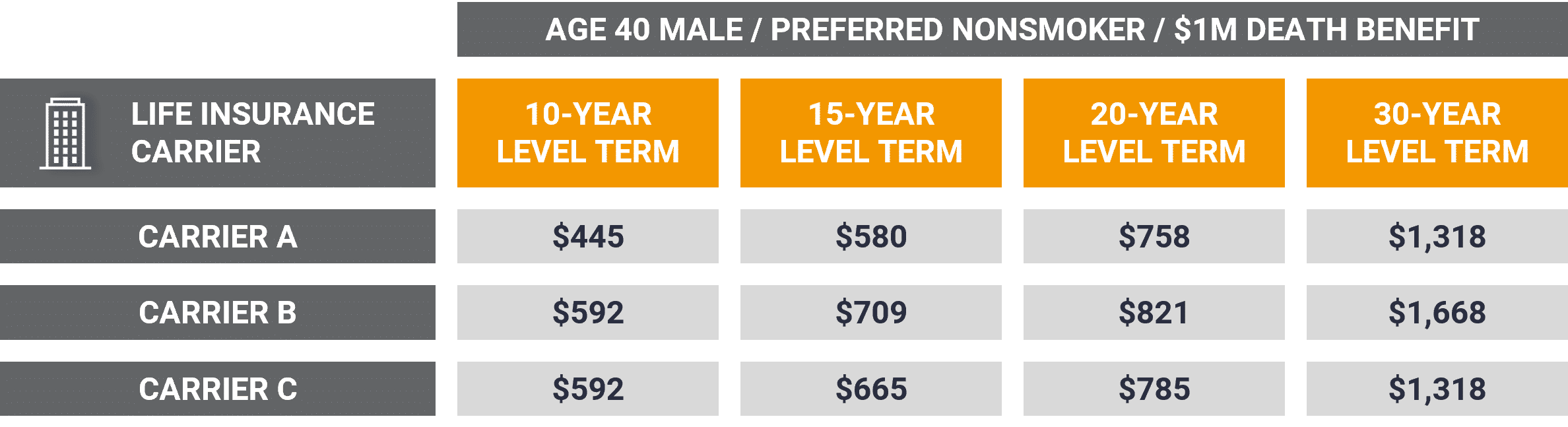

Our term life options include 10, 15, 20, 25, 30, 35, and 40-year plans. The most preferred kind is level term, implying your repayment (premium) and payout (death advantage) remains level, or the same, up until the end of the term duration. This is one of the most straightforward of life insurance policy choices and requires very little upkeep for policy proprietors.

Best Level Term Life Insurance

For example, you might provide 50% to your spouse and divided the rest amongst your adult youngsters, a moms and dad, a good friend, or also a charity. * In some circumstances the death benefit may not be tax-free, discover when life insurance policy is taxed

1Term life insurance coverage offers short-lived protection for a critical period of time and is normally more economical than long-term life insurance coverage. 2Term conversion standards and limitations, such as timing, may apply; for instance, there may be a ten-year conversion advantage for some items and a five-year conversion advantage for others.

3Rider Insured's Paid-Up Insurance coverage Acquisition Choice in New York. There is a cost to exercise this motorcyclist. Not all getting involved policy owners are eligible for returns.

Level Term Life Insurance Calculator

We might be compensated if you click this advertisement. Advertisement Degree term life insurance policy is a policy that supplies the very same survivor benefit at any kind of factor in the term. Whether you pass away on the very same day you take out a policy or the last, your beneficiaries will certainly get the exact same payment.

Plans can likewise last up until specified ages, which in most situations are 65. Past this surface-level information, having a greater understanding of what these strategies require will help guarantee you acquire a plan that fulfills your requirements.

Be mindful that the term you select will certainly influence the costs you spend for the plan. A 10-year level term life insurance policy will cost much less than a 30-year plan due to the fact that there's less possibility of an event while the plan is active. Reduced risk for the insurance company equates to decrease premiums for the policyholder.

Is there a budget-friendly Level Term Life Insurance For Families option?

Your family members's age must also influence your plan term selection. If you have little ones, a longer term makes sense since it safeguards them for a longer time. Nevertheless, if your youngsters are near adulthood and will be economically independent in the future, a shorter term could be a better fit for you than a prolonged one.

Nonetheless, when comparing entire life insurance policy vs. term life insurance coverage, it deserves noting that the last typically prices less than the previous. The outcome is more protection with lower premiums, giving the ideal of both worlds if you require a substantial quantity of insurance coverage yet can not afford a more pricey policy.

What is the difference between Low Cost Level Term Life Insurance and other options?

A degree survivor benefit for a term policy typically pays out as a round figure. When that happens, your beneficiaries will receive the whole amount in a solitary repayment, and that quantity is not taken into consideration earnings by the internal revenue service. Those life insurance profits aren't taxable. Level term life insurance premiums. However, some level term life insurance policy firms allow fixed-period payments.

Rate of interest settlements received from life insurance coverage plans are considered revenue and go through taxes. When your degree term life plan ends, a few different points can take place. Some insurance coverage terminates instantly without alternative for renewal. In various other scenarios, you can pay to expand the strategy past its original day or convert it into a permanent plan.

The downside is that your eco-friendly degree term life insurance will certainly feature greater costs after its initial expiration. Advertisements by Cash. We might be made up if you click this advertisement. Ad For beginners, life insurance can be complicated and you'll have questions you want addressed prior to devoting to any policy.

Why is Level Term Life Insurance For Young Adults important?

Life insurance companies have a formula for determining threat making use of mortality and passion. Insurance providers have thousands of clients getting term life plans at as soon as and use the costs from its energetic policies to pay enduring recipients of various other plans. These business utilize mortality to estimate the amount of people within a specific group will file fatality insurance claims each year, and that information is used to establish average life span for potential insurance holders.

In addition, insurance coverage companies can spend the cash they obtain from premiums and increase their earnings. The insurance firm can invest the money and earn returns - Level term life insurance calculator.

The complying with area information the advantages and disadvantages of degree term life insurance policy. Predictable costs and life insurance coverage Streamlined policy structure Potential for conversion to irreversible life insurance policy Minimal coverage duration No cash money worth build-up Life insurance policy costs can enhance after the term You'll discover clear benefits when contrasting level term life insurance policy to various other insurance coverage types.

What is a simple explanation of Level Term Life Insurance For Seniors?

From the moment you take out a plan, your premiums will never alter, assisting you plan monetarily. Your protection won't vary either, making these plans effective for estate planning.

If you go this route, your premiums will certainly raise but it's constantly good to have some adaptability if you desire to maintain an active life insurance policy policy. Renewable level term life insurance policy is another choice worth taking into consideration. These policies allow you to maintain your present strategy after expiration, supplying versatility in the future.

{kind=link}

Latest Posts

30 Year Term Life Insurance Instant Quotes

End Of Life Insurance Plans

Burial Insurance Reviews