All Categories

Featured

Table of Contents

- – What does What Is Level Term Life Insurance? c...

- – What is the most popular Level Term Life Insur...

- – What types of Level Term Life Insurance Compa...

- – What are the top Level Death Benefit Term Lif...

- – Why should I have Compare Level Term Life In...

- – Who has the best customer service for Level ...

Adolescent insurance coverage gives a minimum of security and could give insurance coverage, which may not be available at a later date. Amounts given under such insurance coverage are generally minimal based on the age of the child. The present limitations for minors under the age of 14.5 would be the greater of $50,000 or 50% of the quantity of life insurance policy effective upon the life of the candidate.

Juvenile insurance policy might be offered with a payor advantage rider, which attends to forgoing future costs on the child's plan in case of the death of the individual that pays the premium. Elderly life insurance coverage, often referred to as graded death benefit strategies, provides qualified older applicants with marginal whole life protection without a medical exam.

The allowable problem ages for this type of insurance coverage range from ages 50 75. The optimum issue amount of coverage is $25,000. These policies are normally more costly than a fully underwritten plan if the individual certifies as a basic threat. This type of insurance coverage is for a small face quantity, commonly purchased to pay the funeral costs of the guaranteed.

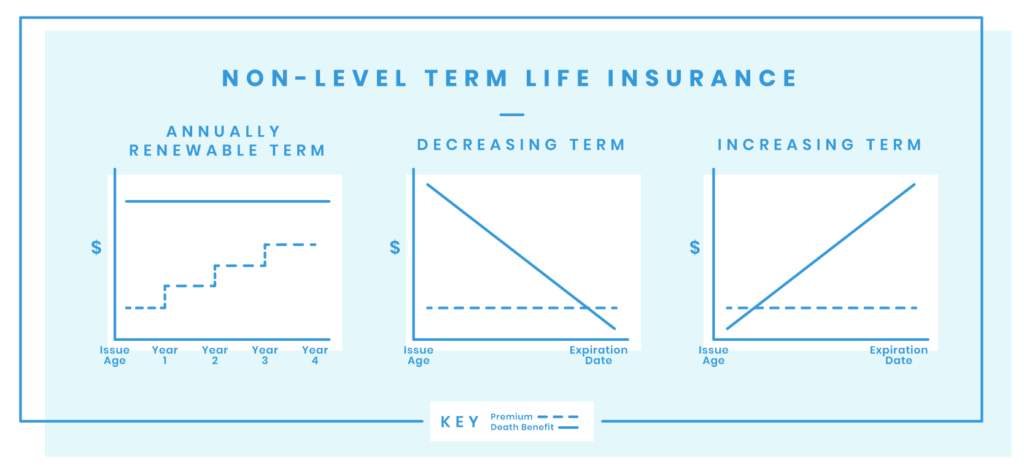

Our term life choices include 10, 15, 20, 25, 30, 35, and 40-year policies. The most popular kind is level term, implying your settlement (premium) and payout (survivor benefit) stays level, or the very same, till completion of the term duration. This is the most simple of life insurance coverage choices and requires extremely little maintenance for policy owners.

What does What Is Level Term Life Insurance? cover?

You can provide 50% to your spouse and divided the rest amongst your adult children, a parent, a pal, or even a charity. No medical exam level term life insurance. * In some circumstances the survivor benefit might not be tax-free, learn when life insurance policy is taxable

1Term life insurance policy supplies momentary security for a vital duration of time and is typically less costly than long-term life insurance policy. 2Term conversion standards and constraints, such as timing, might apply; for example, there may be a ten-year conversion advantage for some products and a five-year conversion advantage for others.

3Rider Insured's Paid-Up Insurance coverage Acquisition Choice in New York City. 4Not available in every state. There is an expense to exercise this cyclist. Products and motorcyclists are available in approved jurisdictions and names and attributes might vary. 5Dividends are not guaranteed. Not all getting involved policy proprietors are qualified for rewards. For choose cyclists, the condition relates to the insured.

What is the most popular Level Term Life Insurance Rates plan in 2024?

We may be made up if you click this ad. Whether you die on the exact same day you take out a policy or the last, your recipients will get the exact same payout.

Plans can also last till specified ages, which in most situations are 65. Past this surface-level information, having a greater understanding of what these plans require will certainly help ensure you purchase a policy that fulfills your requirements.

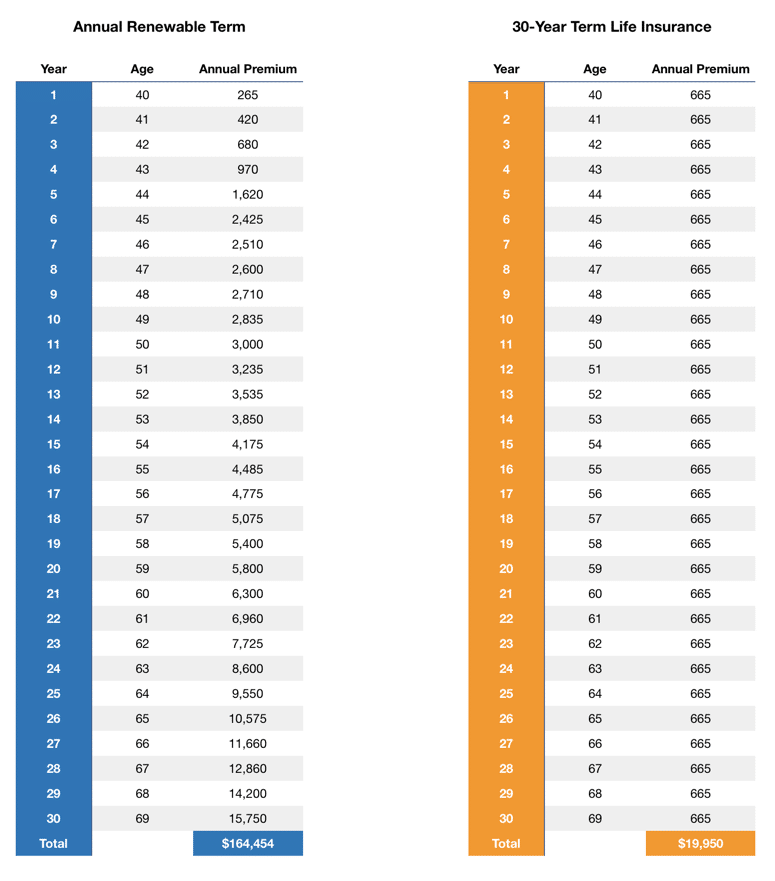

Be conscious that the term you select will affect the costs you spend for the policy. A 10-year level term life insurance plan will cost much less than a 30-year policy due to the fact that there's much less opportunity of a case while the plan is energetic. Lower danger for the insurer relates to lower costs for the insurance holder.

What types of Level Term Life Insurance Companies are available?

Your family members's age need to likewise influence your policy term selection. If you have kids, a longer term makes sense because it protects them for a longer time. However, if your children are near their adult years and will certainly be economically independent in the close to future, a much shorter term may be a better fit for you than an extensive one.

When comparing entire life insurance policy vs. term life insurance policy, it's worth noting that the last commonly costs less than the previous. The result is more coverage with reduced premiums, supplying the very best of both worlds if you need a significant quantity of insurance coverage yet can't pay for a more pricey plan.

What are the top Level Death Benefit Term Life Insurance providers in my area?

A degree survivor benefit for a term plan usually pays out as a lump amount. When that happens, your beneficiaries will get the entire amount in a single repayment, and that quantity is ruled out earnings by the internal revenue service. Those life insurance coverage proceeds aren't taxed. Level term life insurance for families. Some level term life insurance coverage firms allow fixed-period settlements.

Rate of interest payments got from life insurance policy plans are thought about revenue and go through tax. When your degree term life plan runs out, a few various points can take place. Some insurance coverage ends instantly without any option for revival. In other situations, you can pay to expand the plan beyond its initial day or convert it into a long-term policy.

The disadvantage is that your eco-friendly degree term life insurance policy will come with higher costs after its first expiration. Ads by Cash. We may be made up if you click this ad. Advertisement For newbies, life insurance policy can be made complex and you'll have questions you want addressed before dedicating to any plan.

Why should I have Compare Level Term Life Insurance?

Life insurance coverage companies have a formula for determining threat making use of death and rate of interest. Insurers have thousands of customers securing term life policies simultaneously and make use of the costs from its energetic plans to pay making it through recipients of other plans. These firms make use of mortality to approximate the number of people within a specific team will certainly file fatality cases per year, and that details is used to figure out average life expectancies for potential insurance policy holders.

In addition, insurance provider can spend the cash they get from costs and boost their revenue. Since a level term plan does not have cash value, as a policyholder, you can not spend these funds and they don't offer retirement earnings for you as they can with entire life insurance policy policies. Nonetheless, the insurance provider can invest the cash and make returns.

The adhering to area information the advantages and disadvantages of degree term life insurance policy. Predictable costs and life insurance policy protection Streamlined plan structure Possible for conversion to permanent life insurance Restricted coverage duration No money worth accumulation Life insurance policy costs can increase after the term You'll discover clear advantages when contrasting degree term life insurance policy to various other insurance types.

Who has the best customer service for Level Term Life Insurance Policy?

From the minute you take out a plan, your costs will never alter, aiding you plan monetarily. Your coverage will not differ either, making these plans effective for estate preparation.

If you go this route, your costs will enhance but it's constantly good to have some adaptability if you wish to keep an energetic life insurance plan. Eco-friendly degree term life insurance policy is one more alternative worth considering. These policies enable you to keep your present plan after expiry, offering adaptability in the future.

{kind=link}

Table of Contents

- – What does What Is Level Term Life Insurance? c...

- – What is the most popular Level Term Life Insur...

- – What types of Level Term Life Insurance Compa...

- – What are the top Level Death Benefit Term Lif...

- – Why should I have Compare Level Term Life In...

- – Who has the best customer service for Level ...

Latest Posts

30 Year Term Life Insurance Instant Quotes

End Of Life Insurance Plans

Burial Insurance Reviews

More

Latest Posts

30 Year Term Life Insurance Instant Quotes

End Of Life Insurance Plans

Burial Insurance Reviews